The Ripple Effect of Fintech Disruption on Traditional Banking Leaders

The financial technology or fintech industry has been evolving for more than a century now. Driven by remarkable technological innovations, this industry has disrupted the operations of traditional banking for good. Disruption is associated with every digital transformation and with every digital transition, a business ramps up its productivity to reach a successful position.

With this article, we aim to understand fintech disruption and its impact on traditional banking leaders. It will also shed light on how advanced technologies like artificial intelligence and blockchain are converging to drive fintech transformation.

Understanding the Roots of Fintech

Before analyzing the impact of fintech-driven disruption on traditional banking leaders, understanding the roots of fintech is extremely crucial. The banking system went online in the early 1980s with the “home banking services.” The “Homelink” service was launched in the UK in 1983 by the Nottingham Building Society. With this tech-powered innovation, the wave of banking revolution began to sweep through the global banking industry, marking “Homelink Service” as the first true online banking service.

Advancements in the World Wide Web (WWW) led to the introduction of internet banking. Stanford Federal Credit Union offered internet banking to all its members in 1994, and Wells Fargo became the first US bank to add account services to its website in 1995. Although the initial adoption of online banking was slow due to security concerns, it gradually became popular in the late 90s and early 2000s. With the escalated growth of e-commerce and internet availability during this period, financial institutions started to shift their transactions online.

In 1967, Barclays installed its first ATM. During the 1970s, NASDAQ, the world’s first digital stock exchange, and SWIFT, a protocol for facilitating large volumes of cross-border payments between financial institutions, were established. The 1990s saw the first wave of digital banking with the launch of PayPal in 1998, marking the start of new payment systems.

Since 2008, the fintech startup era has spurred innovation among investors and consumers seeking new services. Open Banking has made it easier to create digital banking products. Banks as a Service (BaaS) platforms, such as SolarisBank and Treezor, enable banks and financial institutions to launch neo-banks that enhance customer experience.

Fintech firms have evolved rapidly over the last two decades, securing a position of their own alongside traditional financial institutions. The COVID-19 pandemic has accelerated the fintech industry’s growth and resilience. Now, fintechs lie at the center of the global financial system. According to a KPMG report, global fintech funding was $44.7 billion in the first half of 2025, indicating investors’ interest in funding fintech firms and taking the industry to a new height.

Impact of Fintech Disruption on Traditional Banking Leaders

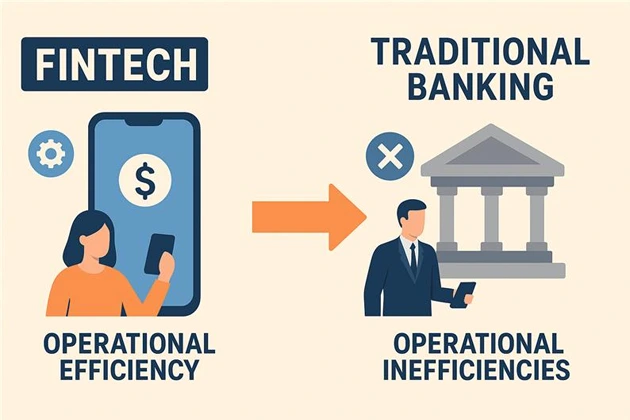

As fintech continues to gain momentum, it is substantially challenging the dominance of traditional financial institutions, including banks, insurance companies, and investment firms. Often characterized by agility, customer-centricity, and innovation, fintech startups are disrupting established business models, making it imperative for traditional leaders to adapt and innovate to remain competitive and retain relevance in this digital age. By offering user-friendly, speedy, and innovative banking services, fintech startups are challenging traditional banking operations.

Traditional banking leaders are now encouraged to upskill themselves and embrace knowledge and skills to use advanced banking technologies. With fintech disruption intensifying competition and eroding market share in key revenue streams like payments and lending, banking leaders are compelled to transition from a physical model to a digitally agile and customer-centric one.

Traditional banks often lack in their IT infrastructure, which slows their decision-making and restricts rapid innovation. Traditional leaders must adapt to changing consumer demands to ensure a 24/7 digital experience for them. To keep up with the industry revolution, banks are investing largely in modernizing their IT infrastructure, opting for a co-existing model, partnering or acquiring fintech firms to integrate innovative technology. With the establishment of innovation labs and venture capital arms, banks are promoting in-house creativity and innovation. Leaders are now pivoting from a product-centric to a customer-centric approach by leveraging data analytics to deliver personalized financial solutions and products. Traditional banks are proactively engaging with regulators to help reshape evolving policies to manage compliance efficiently.

AI and Blockchain in Fintech Transformation

Artificial intelligence and blockchain are two key advanced technologies that have contributed to the global fintech transformation. To assess the influence of AI and blockchain convergence in fintech transformation, we need to evaluate how these two technologies are changing the face of traditional banking operations. The convergence of AI and blockchain creates a synergistic effect within the fintech industry, enhancing efficiency, security, automation, and transparency. Below are the combined impacts of both technologies in the fintech transformation-

● AI swiftly scans mountains of transaction data, spotting suspicious patterns and anomalies. Meanwhile, blockchain locks each transaction into a transparent, tamper-resistant ledger, making data manipulation nearly impossible. When combined, these technologies form a powerful shield against fraud, always one step ahead of threats.

● AI can be embedded within smart contracts to incorporate real-time data analysis and dynamic decision-making. Blockchain ensures secure automated agreements. When combined, these technologies can design smarter, highly efficient, and more adaptable automated financial agreements.

● AI automates daily tasks, and blockchain eliminates intermediaries. At the convergence of these two technologies lies a cost-effective and time-bound transaction system, especially for cross-border payments.

● With AI, fintech firms can analyze consumer behavior and financial patterns to offer tailored recommendations. Blockchain supports decentralized identity management systems, allowing users control over their data. Together, they create a more inclusive financial ecosystem with personalized, accessible, and secure services for users.

The Silicon Journal, as an emerging business magazine in the USA, has been delivering insights and trends of industries like fintech, technology, and others to empower its readers. With The Silicon Journal, one can get well-researched and expert-backed information on various trending topics in the form of articles, news, and blogs. Stay hooked to this business publication to get recent updates on the latest technologies, innovations, industries, trends, and other business aspects.

Related Articles

Recent Articles

Latest Issue